%201.svg)

HIPAA Compliance Checklist for 2025

As the corporate landscape has changed, accountability is no longer optional but a necessity. When executives sign off on financial statements, investors, employees, and regulators expect accuracy and integrity. That’s where SOX Section 302 comes in.

Introduced under the Sarbanes Oxley Act of 2002, SOX 302 requires CEOs and CFOs to personally certify the accuracy of their company’s financial disclosures. The SOX controls were designed to restore public trust after scandals like Enron and WorldCom shook market confidence.

Unlike technical compliance checklists, section 302 SOX ties leadership directly to financial transparency and accountability. This article discusses what SOX 302 certification means, its benefits, and the best practices for compliance.

What is SOX 302?

Section 302 of the Sarbanes-Oxley Act requires CEOs and CFOs to personally certify financial reports. They must ensure statements are accurate and internal controls are reliable.

This certification makes top executives accountable for reporting errors, fraud, or weaknesses in internal controls. It ensures leaders actively review company finances.

SOX 302 enhances transparency in financial reporting and strengthens investor confidence by promoting executive integrity. Investors can trust certified reports more confidently.

By shifting responsibility from auditors to management, SOX 302 reinforces SaaS governance. Executives bear direct responsibility for financial accuracy and controls in SaaS or public companies.

What are the Advantages of SOX 302 Compliance?

SOX 302 compliance boosts investor confidence by ensuring greater transparency and accuracy in financial reporting. Executives are required to personally certify disclosures, increasing corporate accountability and deterring common causes of data breaches.

1. Building Investor Trust and Market Confidence

One of the biggest advantages of SOX 302 compliance is the trust it builds with stakeholders. When executives certify financial statements, investors and markets gain assurance that the company’s disclosures are accurate and reliable.

Transparent Leadership Accountability

SOX 302 certification compels CEOs and CFOs to personally vouch for the accuracy of financial reports, reinforcing investor trust in corporate governance.

Stronger Market Reputation

Companies with robust compliance records are seen as more trustworthy in the marketplace. This often translates into higher valuations and a competitive edge when attracting new investors.

Improved Investor Confidence

Strong section 302 SOX compliance practices reassure investors that risks are managed effectively. According to PwC’s 2024 Global Investor Survey, 87% of investors consider governance and transparency as critical factors in their decision-making.

2. Strengthening Internal Controls Across the Business

Another key advantage of SOX 302 compliance is how it pushes companies to strengthen internal controls, ensuring that risks are addressed before they escalate. Here’s how enterprises benefit:

- Establishes clear procedures for monitoring financial data.

- Reduces the risk of fraud and reporting errors.

- Improves accountability within finance and operations teams.

- Enhances coordination between departments for IT compliance readiness.

- Ensures timely detection and resolution of control deficiencies.

3. Reducing Fraud and Financial Misstatements

Financial scandals often stem from unchecked reporting practices and lack of accountability at the executive level. Sarbanes Oxley 302 directly addresses this by addressing accuracy of financial disclosures.

SEC Chairman Christopher Cox once noted,

“Sarbanes-Oxley helped restore trust in U.S. markets by increasing accountability, speeding up reporting, and making audits more independent.”

For example, Kraft Heinz paid a $62 million penalty in 2021 after misreporting earnings through improper supplier contracts, exposing the cost of neglecting section 302 SOX compliance certification.

4. Improving Corporate Governance and Accountability

Strong corporate governance is a foundation for sustainable growth. SOX 302 strengthens this foundation by setting higher standards for leadership accountability and transparent decision-making.

Executive Accountability

CEOs and CFOs must certify financial statements, ensuring leadership takes direct responsibility for reporting accuracy and ethical oversight. This accountability reduces the SaaS security risks of misleading disclosures.

Ethical Culture

When leaders prioritize compliance, it sets a clear example across the business. Employees follow controls more diligently, creating a culture of integrity and responsibility.

Board Oversight

Boards and audit committees gain deeper visibility into financial controls. This oversight improves decision-making and limits the risk of governance failures.

Regulatory Alignment

Transparent reporting helps organizations stay aligned with SOX certification requirements. Consistent SaaS compliance reduces the likelihood of fines, penalties, or reputational damage.

What SOX 302 Audit Process Enterprises Should Follow?

Enterprises must establish and maintain strong internal controls as the foundation for SOX 302 compliance. A clear process should begin with security risk assessments, control testing, and the definition of internal certification steps.

Step 1: Create Strong Internal Controls

Every SOX 302 audit begins with internal controls, since they form the backbone of accurate reporting. These controls help prevent errors, detect irregularities, and ensure financial data reflects true business performance.

Strong internal controls not only support compliance but also build organizational discipline. When designed well, they streamline audits and make later steps far more effective.

Step 2: Document All Financial Processes Clearly

Clear documentation is essential for any SOX 302 audit. Without it, even well-designed controls may fail under scrutiny. Documentation ensures consistency, creates accountability, and provides auditors with a reliable trail to evaluate.

To make this step effective, enterprises should:

Map Every Process

Outline revenue flows, expense management, payroll, and reconciliations. This makes financial activities transparent and easy to track.

Define Roles and Responsibilities

Specify who approves, records, and reviews transactions. Role-based access control eliminates overlap and accountability gaps.

Standardize Reporting Templates

Use consistent formats for policies, process notes, and financial statements. Standardization avoids confusion and speeds up audits.

Maintain Audit Trails

Record every approval, adjustment, and review in a traceable way. This creates strong evidence of compliance during audits.

Step 3: Conduct Management’s Quarterly Review

SOX 302 certification requires company executives, typically the CEO and CFO, to personally certify the accuracy of quarterly financial reports. This review demands a careful evaluation of internal controls, disclosures, and reported numbers.

During the process, management examines whether controls operated effectively throughout the quarter, identifies any material weaknesses, and ensures disclosures align with SEC standards. If discrepancies surface, they must be addressed before certification.

Step 4: Collaborate With External Auditors Effectively

Effective collaboration with external auditors is vital to ensure the SOX 302 audit process is both rigorous and efficient.

As Keith Higgins, former head of the SEC’s Division of Corporation Finance, aptly put it:

“The strongest approach to deterring and detecting fraud involves collective action from multiple financial stakeholders, which underscores the important roles played by company management, audit committees, external audit firms and regulators.”

By engaging external auditors early, companies can align expectations, reduce scope creep, and focus on high-risk areas. SOX 302 also ensures that both management and auditors operate from a shared understanding.

Mandatory SOX Section 302 Certification Requirements

SOX Section 302 requires CEOs and CFOs to personally certify quarterly and annual financial reports submitted to the SEC. Executives must confirm that financial statements are accurate and internal controls over financial reporting are effective. Here are SOX certification requirements to consider:

1. Why CEOs and CFOs Must Personally Sign Off

Under SOX Section 302, the responsibility for financial accuracy doesn’t just fall on the accounting team. Instead, it places CEOs and CFOs at the center of accountability by requiring their personal certification of quarterly and annual reports.

The rationale is simple: leadership must stand behind the integrity of their financial disclosures. By signing off, executives confirm that they have reviewed the reports, verified their accuracy, and ensured no misleading statements are included.

A notable example comes from the Enron scandal, where executives distanced themselves from misleading financials. SOX 302 certification eliminated that loophole by mandating direct accountability at the highest level.

2. Reporting on Internal Control Effectiveness

SOX compliance certification requires that executives not only vouch for financial accuracy but also certify the effectiveness of internal controls. This ensures that systems designed to prevent errors or fraud are actively tested and maintained.

- Executives must evaluate internal controls every quarter.

- Any weaknesses in the access control must be documented.

- Certification must include details on how controls were tested.

- Reports should confirm that controls are designed to detect fraud.

- Updates are required if new risks emerge during the quarter.

This structured reporting helps regulators and investors trust that the company is actively safeguarding its financial integrity.

3. Disclosing Fraud and Deficiencies Without Delay

Transparency is central to SOX 302 compliance. Companies must immediately disclose any fraud, control failures, or material deficiencies that could impact financial reporting. Delayed reporting in SOX compliance certification not only violates regulations but also affects investor confidence.

Immediate Fraud Disclosure

Executives are required to report fraudulent activities promptly, ensuring stakeholders are not misled by hidden risks.

Control Weakness Reporting

Any significant deficiency in internal controls must be highlighted, along with its potential financial impact.

Timely Communication

Disclosures must be made without delay, whether through SEC filings or direct investor updates.

Corrective Action Plans

Reports should also outline steps management is taking to address the identified issues.

Executive Accountability

CEOs and CFOs remain personally liable for omissions or delays, even if lower teams identify the problems first.

4. Meeting Quarterly Certification Obligations

SOX 302 makes quarterly certifications a non-negotiable requirement for public companies. Every three months, CEOs and CFOs must review and confirm the accuracy of financial statements, evaluate internal controls, and certify compliance.

This recurring process ensures that accountability isn’t limited to year-end reporting but is consistently maintained throughout the year. By requiring frequent sign-offs, regulators keep pressure on leadership to maintain transparency, accuracy, and strong governance practices at all times.

Some Common Challenges of Sarbanes Oxley Section 302

SOX 302 aims to improve corporate accountability but introduces several compliance challenges for enterprises. These often arise from the complexity of financial systems and evolving business structures.

1. High Costs of Ongoing Compliance and Audits

One of the major challenges companies face with SOX 302 is the financial burden of maintaining ongoing compliance. Regular audits, internal control assessments, and executive certifications require significant investments in staff, training, and technology.

For many enterprises, these costs can run into hundreds of thousands of dollars annually, especially for smaller firms with limited resources. Despite the expense, failing to invest adequately can lead to even higher costs in penalties, reputational damage, or financial restatements.

2. Managing Endless Documentation and Reporting

SOX 302 requires detailed records of every financial transaction, internal control test, and executive review. For many enterprises, maintaining this level of documentation can feel overwhelming and time-consuming, especially when teams juggle multiple reporting systems.

To manage the workload effectively, enterprises often focus on these key practices:

- Centralize Documentation: Store all compliance-related records in a single, accessible system to streamline audits.

- Standardize Templates: Use uniform reporting formats for policies, processes, and financial statements.

- Automate Where Possible: Implement software tools to track approvals, control testing, and certification sign-offs.

- Regular Internal Reviews: Conduct ongoing reviews to catch gaps early and avoid last-minute reporting crunches.

- Train Teams Consistently: Ensure all employees understand documentation requirements and reporting deadlines.

3. Identifying Hidden Risks Before They Escalate

Proactively identifying hidden risks is one of the toughest challenges in SOX 302 compliance. Companies must constantly evaluate processes, transactions, and controls to catch potential issues before they become material weaknesses.

Regular Risk Assessments

Conduct frequent risk assessments across all financial processes. This helps uncover areas that may be vulnerable to errors, fraud, or control gaps before they escalate.

Cross-Department Collaboration

Engage multiple departments in risk identification to gain a comprehensive view. Different teams often spot risks that others might overlook, improving overall compliance coverage.

Monitoring Key Indicators

Track key performance and compliance indicators in real time. Early warning signs, such as unusual transactions or delays in approvals, can prevent small issues from becoming serious problems.

Leverage Technology Tools

Use automation and analytics to detect anomalies or potential fraud patterns. These tools help identify hidden risks faster than manual reviews, reducing the likelihood of oversight.

Prompt Corrective Action

Once a risk is identified, implement corrective measures immediately. Addressing issues proactively minimizes regulatory exposure and protects both financial integrity and stakeholder confidence.

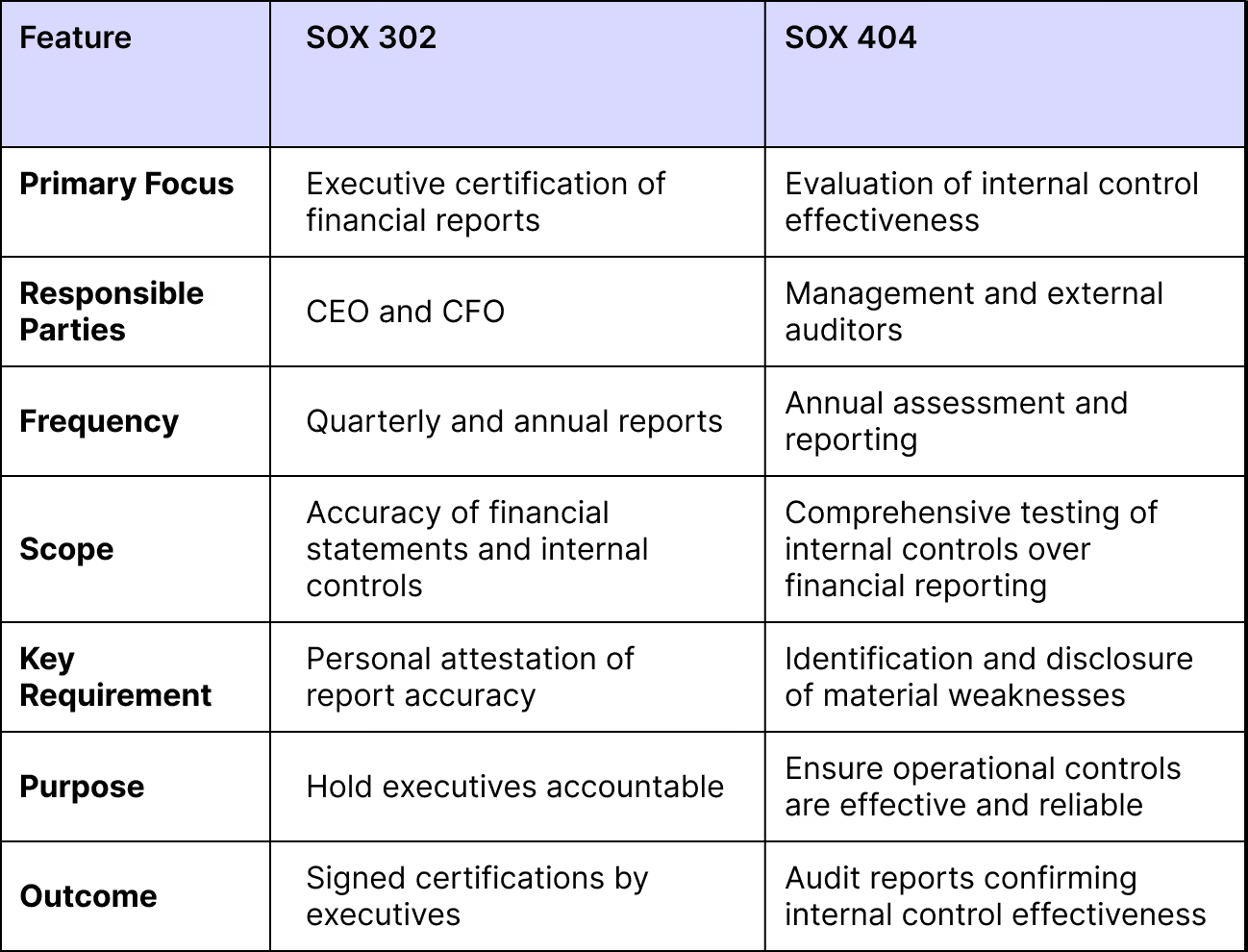

What is the Difference Between SOX 302 and 404?

SOX 302 requires CEOs and CFOs to personally certify the accuracy and completeness of financial reports. It focuses on executive accountability for financial disclosures.

SOX 404 mandates companies to establish, document, test, and report on the effectiveness of internal controls over financial reporting. This section often involves independent annual audits to assess the control systems.

In simple terms, SOX 302 vs SOX 404 centers on personal certification by top executives. SOX 404 emphasizes independent evaluation of internal control frameworks.

Together, these sections provide a dual layer of financial governance: leadership accountability paired with operational control assessment.

How CloudEagle.ai Can Help Enterprises Stay Compliant?

CloudEagle.ai is a SaaS management and procurement platform designed to help you track, optimize, manage, and renew your SaaS licenses efficiently.

With CloudEagle.ai, you can detect potential risks, enforce security policies, and effortlessly generate audit-ready reports. Here’s how it can help your company stay compliant.

Centralized Compliance Management

Non-compliance can lead to costly fines and legal complications, but CloudEagle.ai helps you stay ahead by ensuring continuous access control and compliance. With real-time alerts, you can detect potential violations early and address them before they result in penalties.

CloudEagle.ai provides a centralized platform to monitor user activity, track application access, and maintain detailed records. By simplifying compliance risk management, it reduces complexity and enhances efficiency.

With built-in support for key regulations like ISO 27001, SOC 2, and GDPR, CloudEagle.ai streamlines access control, monitoring, and auditing. This eliminates the need for multiple tools, making compliance oversight more effective and hassle-free.

Automated Compliance Reporting

Generating compliance reports manually can be time-consuming, but CloudEagle.ai automates the process, ensuring audit-ready reports are always available. This not only saves time but also reduces manual effort.

Real-time audit logs provide complete visibility into access events and application usage, allowing you to monitor activity and address any compliance concerns swiftly.

Continuous Monitoring and Risk Management

With real-time monitoring of user access and data transactions, CloudEagle.ai ensures your security controls remain effective. By continuously overseeing activity, your company can quickly detect and resolve security gaps before they escalate.

The platform also identifies compliance gaps early, offering actionable insights to mitigate risks proactively and helps with SaaS security posture management.

Automated Access Reviews

Regulations like SOC 2 and ISO 27001 audit require regular user access reviews, which can be tedious without automation. CloudEagle.ai streamlines this process by continuously tracking and validating user access, ensuring only authorized individuals can interact with sensitive data.

By automating access reviews, the platform minimizes manual work, reduces non-compliance risks, and strengthens regulatory adherence.

Audit Trails for Seamless Compliance

Maintaining detailed audit trails is essential for SOC 2 and ISO 27001 compliance. CloudEagle.ai records all system activities, ensuring data integrity and making it easy to retrieve evidence during audits.

Additionally, the platform enforces security policies aligned with ISO 27001, GDPR, and SOC 2 audit. You can customize policies to fit your company’s specific compliance needs, ensuring ongoing regulatory adherence.

Conclusion

SOX 302 ensures financial transparency and holds executives accountable for accurate reporting. While compliance can be challenging, strong internal controls and proactive risk management make it manageable.

By following best practices, companies not only meet regulatory requirements but also build investor trust and strengthen governance.

Schedule a demo with the experts at CloudEagle.ai today to streamline your SOX 302 compliance and safeguard your enterprise’s financial integrity.

FAQs

1. What does SOX 404 stand for?

SOX 404 refers to Section 404 of the Sarbanes-Oxley Act, which ensures reliable internal controls. It requires management and auditors to assess control effectiveness and report material weaknesses publicly.

2. What questions are asked in the SOX 302 certification?

Executives must certify that financial statements are accurate and reflect all transactions fairly. They also confirm internal controls work effectively and that any fraud or deficiencies are disclosed.

3. Is SOX compliance mandatory?

Yes, all publicly traded companies in the U.S. must comply with SOX regulations. Compliance ensures CEOs and CFOs are accountable for financial accuracy and transparency in reporting.

4. What is the penalty for violating the SOX?

Violations can lead to significant fines, executive imprisonment, and reputational damage for the company. The SEC may also investigate, potentially triggering shareholder lawsuits and additional financial penalties.

5. How much does SOX compliance cost?

Costs depend on company size, reporting complexity, and internal control systems. Mid-sized firms often spend hundreds of thousands yearly on audits, controls, and compliance technology.

6. Who falls under SOX compliance?

All publicly traded U.S. companies are subject to SOX compliance, including CEOs, CFOs, and finance teams. Anyone responsible for preparing, certifying, or auditing financial reports must adhere to these regulations.

.avif)

.avif)

.avif)

.png)